“The high tax burden… and frequent changes in the rules of the game have eroded competitiveness.”

Ramiro Costa is General Manager of the Buenos Aires Grain Exchange, where he coordinates teams specialized in economics and agribusiness. He also serves on the boards of organizations such as Argentrigo, Asagir, Maizar, Acsoja, and the Argentine Agroindustrial Council. Costa is an economist with extensive experience in economic analysis and in the development of agroindustrial value chains.

Ramiro Costa, General Manager of the Buenos Aires Grain Exchange.

AgriBrasilis – How do you assess Argentine agribusiness?

Ramiro Costa – I would assess Argentine agribusiness as one of the strategic pillars and most competitive sectors of the national economy. It is a sector with high productivity, strong technological adoption and solid integration into international markets, which makes it a central actor in generating foreign exchange, employment and economic activity throughout the entire value chain.

Argentina has extensive areas with high agricultural suitability, allowing for globally competitive yields. In addition, there is a high level of technological adoption: practices such as no-till farming, biotechnology applied to seeds and precision agriculture have helped improve efficiency and sustain productivity. The agro-industrial complex, especially in soybeans and corn, also presents efficient integration between production, processing and exports.

However, the sector operates in a challenging macroeconomic environment. Economic volatility, a high tax burden, including export duties, and certain logistical infrastructure limitations affect its competitiveness.

AgriBrasilis – What are the main obstacles facing the sector?

Ramiro Costa – The main obstacles facing Argentine agribusiness are not related to its productive capacity, but rather to the environment in which it operates. The main constraint has been macroeconomic instability: high inflation, exchange rate volatility and difficulties in accessing financing affect planning and increase the cost of working capital, which is essential in an input-intensive activity.

In addition, for long periods there have been tax and regulatory distortions. The high tax burden, including export duties, together with exchange rate misalignment and frequent changes in the rules of the game, have eroded competitiveness and affected farmers’ margins. Logistical infrastructure limitations also persist, generating additional costs that, in many regions, reduce the competitiveness of the production system.

AgriBrasilis – Is there a risk of greater pressure on prices and margins in Argentina?

Ramiro Costa – In terms of international prices, Argentina is a price taker, meaning its evolution depends on the global cycle: the supply from major producers such as the United States and Brazil, import demand and international financial conditions. Geopolitical issues are also increasingly interconnected with trade and the formation of commodity prices.

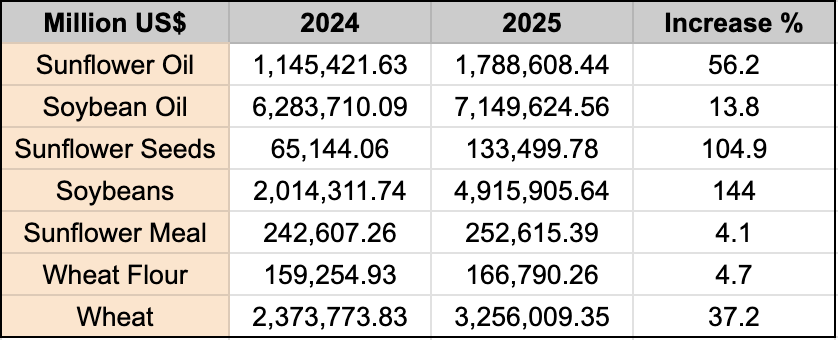

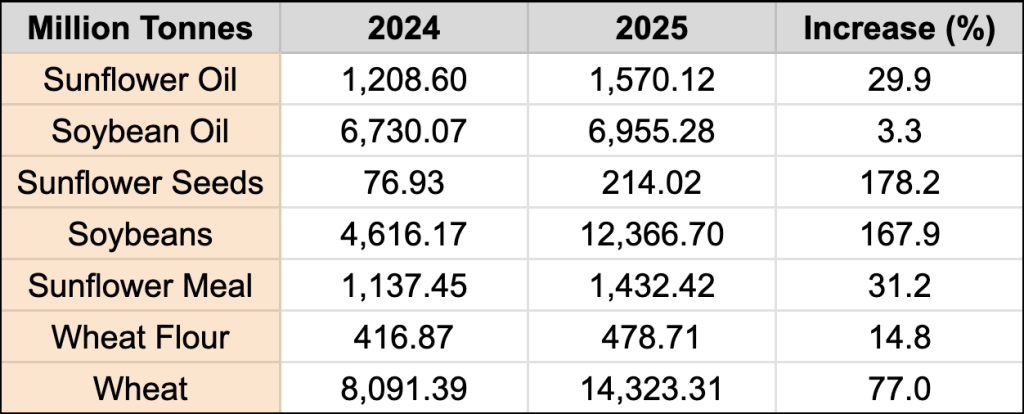

AgriBrasilis – What factors explain the 25% growth in exports in the last harvest?

Ramiro Costa – The growth in exports in the last harvest is mainly explained by a record production, particularly of wheat, sunflower and soybeans. Improved weather conditions compared to the previous harvest, which was marked by drought, allowed yields to recover and, consequently, increased the exportable volume.

Internationally, the context was also favorable. A tighter supply in some grains and dynamic demand from markets such as China and countries in Southeast Asia helped sustain exports.

This was also accompanied by internal factors, such as an improvement in the effective exchange rate for exporters, reductions in export duties and progress in deregulation measures affecting the sector.

Argentina: Oil and Grain Exports in 2024 and 2025 (US$ millions)

Argentina: Oil and Grain Exports in 2024 and 2025 (million tonnes)

AgriBrasilis – What are the prospects for grain production in the next season?

Ramiro Costa – The outlook for grain production in the coming seasons remains favorable. For the 2025/26 season, estimates from the Bolsa de Cereales de Buenos Aires project total production close to 142.5 million tonnes, with emphasis on corn (57 Mt) and soybeans (48.5 Mt), in addition to contributions from crops such as wheat and sunflower.

AgriBrasilis – What is expected from the Mercosur–European Union agreement?

Ramiro Costa – It is expected that the Mercosur–European Union Agreement will represent a turning point in the international integration of the bloc, particularly for Argentina’s agro-industrial chain. In a global context of increasing protectionism, the agreement would open more predictable access to the market of the European Union, one of the largest markets in the world.

This would occur through tariff reductions for most agro-industrial products and the creation of quotas for strategic goods such as meat. In this way, Mercosur could compete under better conditions in a market where Argentina still has a relatively small share.

In addition, the agreement would bring greater regulatory predictability, helping to stimulate investments and improve the competitiveness of the bloc and its agro-industry.

Read more:

Environmental Requirements, Trade Barriers and Risks for Brazilian Agribusiness