“…the agility of startups, associated with greater risk tolerance and adoption of cutting-edge technology, transforms the way in which new technologies are produced…”

Martha Delphino Bambini, innovation analyst at Embrapa

Maria Beatriz Machado Bonacelli, professor at Unicamp

Martha Delphino Bambini is an innovation analyst at Embrapa Agricultura Digital (Embrapa Digital Agriculture), working in areas of open innovation, articulation of partnerships and relationships with startups and innovation and entrepreneurship ecosystems. Bambini is a master with a Ph.D in scientific and technological policy, specialist in business administration from FGV-SP and chemical engineer from the State University of Campinas.

Maria Beatriz Machado Bonacelli is is a professor at the Graduate Program in Scientific and Technological Policy at State University of Campinas and president of the Management Contract Evaluation Committee between the National Center for Research in Energy and Materials and the Ministry of Science, Technology and Innovation. She graduated with a Ph.D in economic sciences from State University of Campinas and Université des Sciences Sociales de Toulouse, France, respectively, and specialized in economics of the agrifood system.

Since the 2000s, a wave of agricultural innovations has transformed the agri-food value chain through the convergence of several technological fields: biology, agronomy, plant and animal science, digitalization and robotics. Adoption of digital technologies in agricultural research activities and on rural properties contributes to productivity gains, resilience and sustainability, elimination of waste and increased efficiency in logistics and marketing, offering greater transparency and reliability to production chain activities, from the farm to the consumer’s table.

The new entrepreneurial movement based on technologies applied to agriculture – called AgTech, AgriTech, AgroTech or AgriFoodTech – has contributed to the dynamics of agricultural innovation. The agility of startups, associated with their greater risk tolerance and adoption of cutting-edge technology, transforms the way in which new technologies are produced and value is generated in agriculture.

AgTechs are becoming central to open innovation processes, establishing partnerships with corporations in the agricultural sector, cooperatives, research institutes and universities, as well as other startups and large companies in the digital and telecommunications sector.

As a result, a new dynamic emerges, structured from innovation ecosystems, which includes organizations that generate new ventures, such as business incubators and accelerators and venture capitalists, essential to offer knowledge, good practices and resources for the development of new companies.

This collaborative context leads to the development and diffusion of new products and services for producers and other links in the agricultural chain, based on the use of new converging technologies and expansion of mechanisms for connectivity in the field.

The AgriFoodTech segment is divided into two branches: “AgTech”, with a focus on technological solutions involving input, production and logistics and “FoodTech”, associated with inputs and technologies for agribusiness, new foods and new models of product commercialization. AgriFoodTech refers to the set of these segments, from the farm to the consumer’s plate, but often the nomenclature “AgTech” continues to be used in a simplified way.

Global strengthening of the AgTech segment started in 2013 and, in 2020, a new inflection point was observed, motivated by startups that benefited from opportunities arising from covid-19.

With regard to Venture Capital investment, the AgFunder report highlights a growth of 85% between 2020 and 2021. Segments with the greatest progress were those that met demands that arose in the pandemic, such as the online sale of food, which grew 188% in the period, receiving more than a third of the sector’s investments. Other categories that doubled their investments were innovative food, online restaurants and meal kits, and “cloud” retail infrastructure. New production systems, especially vertical farms and indoor farming, are also expected to increase investments in 2022.

The Startup Genome report (2022) highlights some sub-segments of the AgTech market that have been attracting investor interest. Consumers continue to seek more sustainable food sources, especially involving alternatives to animal protein. In 2021, there was a growth in early-stage entrepreneurship both in alternatives to meat – both cultured and uncultivated – and in relation to vegan products.

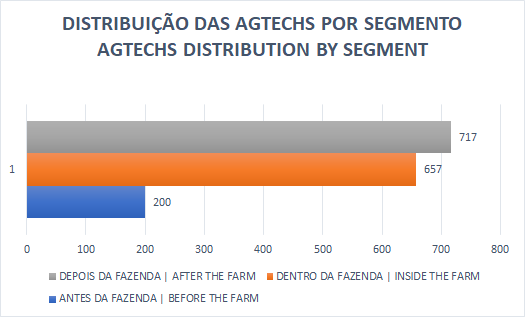

Distribution of AgTechs by segment (SOURCE: Radar AgTech)

There are sub-segments in the field of AgriFoodTech showing growth and consolidation trends. CleanTech and GreenTech involve sustainable, ecological and environmental solutions, with innovative ideas and concepts. ClimaTech refers to startups created to fight climate change. FarmTech covers the segments of digital agronomy, production, planning and decision support, logistics, market access and financing.

Global agriculture challenges for greater sustainability and for methods of adaptation and mitigation of climate change represent an opportunity and a gap to be filled by CleanTechs, GreenTechs and ClimaTechs.

Another sub-segment is AgroFinTech, formed by startups that facilitate financial transactions and access to credit for farmers or other agribusiness companies, usually relying on digital mechanisms. In general, these segments follow a multidisciplinary approach, adopting Artificial Intelligence, Big Data and Analytics techniques and Industry 4.0 practices.

It can be said that the multidisciplinary nature and sub-segmentation in the AgriFoodTech market are signs of maturity that the sector has been acquiring, increasingly supported by specialized incubators and accelerators, with more investors and investment modalities.

The mapping of Brazilian startups conducted by Radar AgTech highlights categories of solutions developed for the production chain – farm management systems, systems integrator platform, drones, machines and equipment and remote sensing, diagnostics and image monitoring – and post-production, especially the innovative food categories and new food trends and marketplaces and platforms for trading and selling agricultural products. These five categories represent about 51% of the AgTechs mapped.

The Distrito study corroborates this view, highlighting the prevalence of solutions for precision agriculture, in particular, agricultural production management software, applications in the internet of things and big data analytics for the field. Applications in biotechnology, automation and robotization and marketplace solutions also stand out.

The panorama points to a space for growth in the segment as a whole, based on an increase in investor interest and confidence. Startups focused on new production systems have a high investment perspective, involving technological urban farming and new forms of production, having stood out for their pioneering spirit and attracted attention to new investments.

Brazil is currently the 6th largest market in terms of Venture Capital investments in AgTechs, behind the United States, China, India, Germany and the United Kingdom. The Distrito report also highlights that the growth of startups focused on agricultural innovation has been organic, with no major efforts directed towards the foundation of new AgTechs. However, it is necessary to consider the strengthening of incubators and accelerators specialized in the AgTech segment, as well as innovation hubs and specialized investment funds – international and national – operating in Brazil. This specialized support structure is a factor that contributes to the development and growth of startups in the sector.

The Brazilian market has several characteristics that can benefit the AgTech segment, including: the relevance of the agricultural sector to the Brazilian economy (27.4% of the Brazilian Gross Domestic Product, the highest percentage since 2004); the importance of its domestic market and the sector’s exports; its pioneering spirit and scientific competence in tropical agriculture; together with the strengthening of the Brazilian agricultural innovation ecosystem based on the structure to foster entrepreneurship and institutional support from government sectors.

This combination of conditions has potential for good results in the national market and to enable Brazilian startups to advance into new markets, especially in Latin America, as well as encourage mergers and acquisitions between startups and large companies operating in AgriFoodTech.

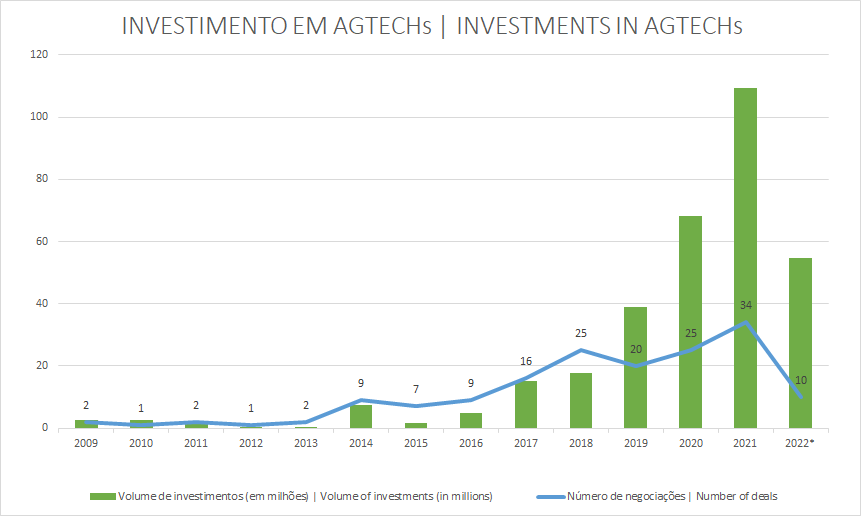

Amount of investments on AgTechs (SOURCE: Radar AgTech)

READ MORE: